Bangalore, June 11, 2025 — India’s residential property market has experienced a remarkable surge, with prices across major cities climbing nearly 48% over the past five years. The sharpest increase came in Bengaluru, where property values soared by an astounding 79%, driven by post-COVID demand, infrastructure development, and evolving buyer behavior.

Growth Across Cities

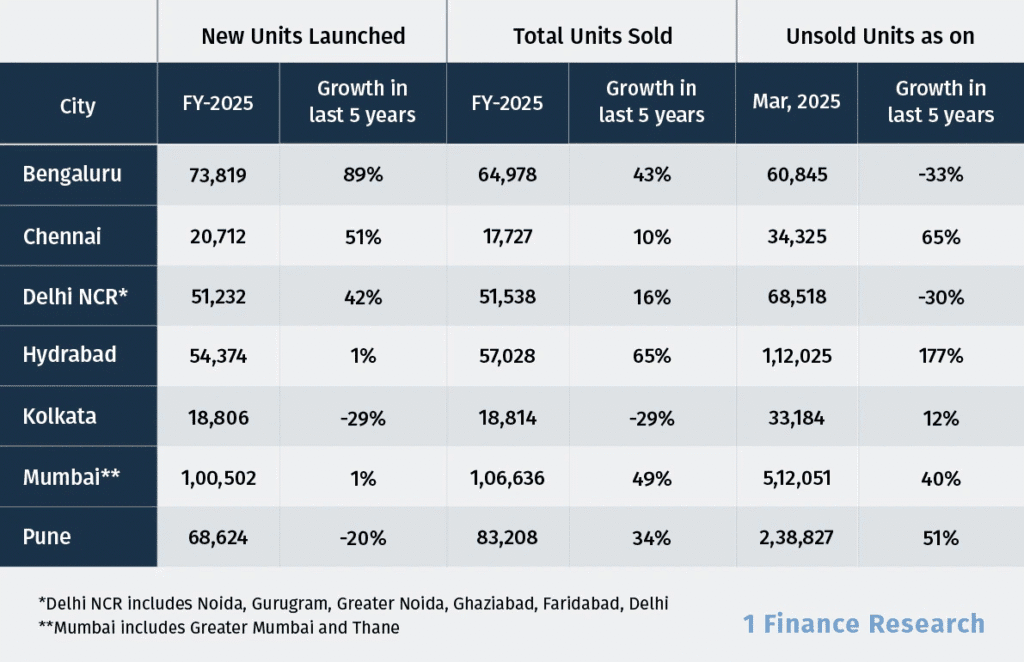

- Bengaluru led the surge with a staggering 79% rise in property prices, supported by strong tech sector growth, infrastructure upgrades like the Namma Metro, and increasing investor interest.

- Mumbai remains the priciest metro, with average rates reaching ₹26,975 per square foot.

- Hyderabad is facing oversupply issues, with a 177% increase in unsold inventory despite rapid urban development.

- Delhi NCR saw a 30% drop in unsold homes, signaling robust end-user demand and improving market stability.

- Chennai experienced a 51% rise in project launches, but sales increased only 10%, indicating a possible demand lag.

- Pune reduced new launches by 20% to balance existing stock.

- Kolkata witnessed a slowdown, with both new launches and sales declining by 29%.

Analysts: From Boom to Balance

Insights from 1 Finance’s All-India Housing Total Return Index show it rising from 167 in 2020 to 247 in 2025, reflecting a 48% growth.

Animesh Hardia of 1 Finance observes a market divide: “Existing homeowners are sitting on appreciated assets, but potential buyers are torn between FOMO and fear of buying at the top.” With cooling prices in some pockets and rising inventory in others, market momentum is transitioning from an aggressive rally to a more moderate pace.

Supply vs Demand

Despite a 32% increase in unsold inventory nationwide, sales have also grown by 33%, while new project launches rose by only 10%. This indicates that demand is still strong and may soon outpace supply in select markets.

Hardia points out that the shift is not a sign of crisis but a move toward equilibrium. As infrastructure projects continue and urban connectivity improves, especially in Tier-1 and peripheral regions, real estate growth is expected to sustain at a healthier rate.

Global Parallels

India’s housing trend mirrors broader global movements:

- Nationwide housing prices are projected to rise around 6% in 2025, though stress is building in luxury segments.

- In the United States, high mortgage rates of around 7% and limited inventory are pushing more people toward renting, creating upward pressure on rental prices.

- Florida offers a cautionary tale, with declining home values due to rising insurance and property tax burdens after a pandemic-fueled boom.

What It Means for Buyers and Investors

- Buy cautiously: Avoid buying out of fear of missing out; market conditions now demand research and patience.

- City-specific strategies: Cities like Bengaluru and Delhi NCR still offer strong fundamentals; oversupplied markets require more scrutiny.

- Affordability is key: Developers focusing on mid-income and affordable segments are likely to see sustained demand.

- Rising rental appeal: In cities where buying is expensive, rental housing demand is gaining momentum, offering investor opportunities.

Bottom Line

India’s real estate market has seen a solid five-year bull run, but the days of unchecked growth may be ending. While some markets are showing early signs of saturation, others continue to benefit from strong fundamentals and infrastructure support. The shift toward a more stable and sustainable property market may favor long-term investors who prioritize fundamentals over hype.